There are only a few opportunities to make a living by getting good at creating tables to facilitate high-frequency math that end-users will find entertaining but will have predictable statistical properties at scale.

One of them is designing roleplaying games. Seems like an interesting topic but someone else will have to write about it. In this column, the dragon sleeps on a hoard of interchange revenue, you slay him to get credit cards rewards points, and the card issuer running the game merrily chuckles at players’ misperception that they are dragons. No, silly, they’re much realer and much richer.

A disclaimer off the top: I used to work at, and am still an advisor of, Stripe. A major portion of the Stripe economic model is charging businesses money to take payments on credit cards. Stripe’s two largest costs are paying smart people and paying interchange, and of the two, one would feel a lot better to cut.

Another disclaimer: Due to long-standing practice, I am (homeopathically) exposed to the common equity of financial services companies that my family uses, so that I can call up Investor Relations if I ever need to escalate a routine banking issue. My family’s main U.S. bank happens to be Chase, which is mentioned below.

Almost everybody writing about credit cards on the Internet receives some sort of spiff if you sign up after clicking through tagged links in their material. That is not my business model (people pay me to write about financial infrastructure), but is probably one you want to be cognizant of every time you read about credit cards online.

Rebating interchange to earn share of wallet

As we have discussed previously, credit cards have multiple different ways of earning money, but the most important one to this discussion is interchange. It is a fee, ultimately paid by the card-accepting business, which gets sliced up between various parties in the credit card ecosystem to incentivize them to put their logos in the wallets and on the phones of well-heeled customers and increase the amount they spend and the frequency with which they spend it. (In industry, we sometimes distinguish interchange—which mostly goes to the issuing bank—and scheme fees—which mostly go to the credit card brand itself—but as interchange is much larger, let’s just call them both interchange for simplicity.)

Interchange is generally a percentage fee based on the final transaction size plus optionally a per-transaction fee. You can just look up the rates, but I strongly recommend you don’t, as you will be reduced to gibbering madness. (It took many smart people many years of work before Stripe could deterministically predict almost all interchange it was charged in advance of actually getting billed for it.)

To highlight something which is routinely surprising for non-specialists: interchange fees are not constant and fixed. They are set based on quite a few factors (gibbering madness intensifies) but, most prominently, based on the rank of card product you use. The more a card product is pitched to socioeconomically well-off people, the more expensive interchange is. Credit card issuers explicitly and directly charge the rest of the economy for the work involved in recruiting the most desirable customers.

The basic intuition underlying rewards cards as a product is that highly desirable customers have options in how they spend their money. You can directly influence them to use your rails by making those rails more lucrative, more fun, or both for the customer. And so card issuers (and the networks) compete with each other for so-called “share of wallet” by bidding with interchange.

This is not quite as sophisticated as the system of dueling robots which bids for your attention every time you open a page on the Internet with an ad on it. The bids are generally speaking pretty static and made years in advance, at or before the time a user signs up for a card product, with relatively minor adjustments made over time. Program managers at card issuers are extremely, extremely sensitive to upsetting the apple cart and churning loyal users, and so they attempt to avoid doing this except when circumstances make it unavoidable.

Why isn’t every card a rewards card?

Different regions have ended up with different equilibria in the rewards game. In the United States, card acceptance is expensive and the rewards economy is robust. In Japan, card acceptance is expensive and the rewards economy is fairly muted due to—ahem—effective collusion by issuers. In Europe, card acceptance is cheap by regulatory fiat and so rewards are far less common (or commonly lucrative) than in the U.S.

Similarly, debit card rewards used to be fairly common in the United States until the Dodd-Frank Act capped debit card interchange (with a very important carveout for small banks in the Durbin amendment). When interchange is regulated, the size of the pie isn’t large enough to give the end-user of the card a tasty slice, and so they get nothing.

But we can see that, even scoping to credit cards in the United States, not every card is a rewards card. What explains why CapitalOne, for example, offers rewards for its Quicksilver card but not the Platinum Mastercard? Is mercury attempting to burnish its image after that horrible toxicity thing?

Partly, this is that different users have different jobs-to-be-done for credit cards. (Many users of credit cards, potentially including some readers of this column, believe that they are the typical users of credit cards. No users of credit cards are typical.)

Credit cards are both a payment instrument and an access point for a revolving credit line. That they are an expensive way to borrow money is one of the first things said in any personal finance text. They are also one of the most accessible ways to borrow money, and that is their primary value proposition for many users, typically ones lower on the socioeconomic ladder. These users spend relatively little in a month compared to their revolving balance, which they continuously pay interest on. It trivially follows that most money on their accounts is earned via net interest margin and not from interchange.

To the extent these users notice numerically defined features of their credit cards, which is somewhat dubious, it is the headline APR (cost of credit) and their credit limits. “Starter” cards and other products aimed at this user group typically have no rewards; they instead use interchange income to “bid down” the headline APR. Interchange functions as a subsidization of the cost of credit throughout the economy by businesses which want to sell things to people who would use credit to buy things. The limit case of this is Buy Now, Pay Later, where the cost of credit is subsidized straight to free.

The heaviest credit card spenders, and this fact is both uncontroversial and flies in the face of what many personal finance columnists believe, are wealthy and sophisticated. They use credit cards primarily as payment instruments. Issuers compete aggressively for their business, which is quite lucrative. This is not because they pay much in interest, because while they have higher headline APRs they only rarely revolve balances. It is because “clipping the ticket” via interchange on a high volume of transactions is an excellent business to be in.

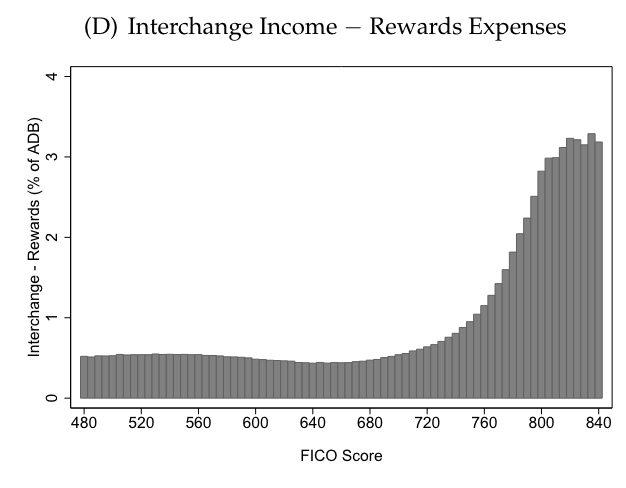

How dramatic is this? Allow me to reproduce a graph from Regulating Consumer Financial Products: Evidence from Credit Cards. (This paper is something of the Rosetta stone for credit card issuance as a field, both in that it is a single source for understanding a huge range of human endeavor and in that it stands in for a very large literature that nobody else reaches for to be the first citation when the Rosetta Stone already exists. If you see an unlabeled graph on Twitter about credit cards, it was probably lifted from this paper.)

As you can see, as a percentage of Average Daily Balance (ADB), even after rewards expense, interchange gets very sharply more lucrative at the top of the credit score distribution (740+, which is roughly 10% of accounts). The difference is actually larger than you see here, since credit lines and ADB also increase with credit score, for predictable reasons. (Rich people consume more than poor people on an absolute basis, film at eleven.)

The complexity spectrum of rewards products

The simplest reward products are straight “cashback”. The issuer totals up all of one’s net purchases (all purchases less refunds) in a statement period. It then credits the user with a particular percentage of that for each statement. Either automatically or periodically at the user’s request, it transforms some of that notional banked credit into a statement credit, decreasing the amount the user needs to pay to cover their purchases in the current month.

This is as simple as it gets and we’re already necessarily handwaving away libraries worth of complexity. (For example, calculation of net purchases needs to be fairly robust against adversarial collaboration of users and merchants or the issuer gets turned into a money pump within a matter of days and will not likely be able to detect or reverse this condition for at least several weeks. This has happened many, many times. Credit card issuers, when they screw this up, lose millions of dollars and dry their tears on money.)

Anyhow, in the mists of history, that percentage started flat; typically, 1%. The math supporting this is typically fairly simple: take in 140bps as revenue, pay the user 100 bps as effectively a cost of customer acquisition, keep some portion of 40 bps as one’s margin.

In nations other than ones with effective cartel-like behavior by issuers, this equilibrium was not stable, because competing issuers would bid e.g. 1.25% cash back on the same underlying economics and compete for share of wallet. This happened extremely robustly, for decades.

One iteration of this game was cash back “categories”. Particularly post-Internet, certain cohorts of customers were most interested in the headline cashback percentage rate. Issuers began to design products which were more complicated, such as “1% cash back in principle, however, 1.5% cash back at gas stations.”

A fun rabbit hole about credit card acceptance

A huge percentage of all credit cards are “co-branded”; they are issued by a financial institution but bear the name of some other institution which inspires a lot of loyalty. A teeny, tiny percentage of co-branded cards name e.g. tertiary educational institutions. Most name a business that a customer has an intense, ongoing relationship with: Costco, their airline of choice, etc.

Co-branded cards are extremely big business. One subtlety about them: a co-branded card will often have a special rewards tier for the business named on the card. This is partially that business choosing, as a marketing expense, to split some of their core margin with their most loyal customers (overwhelmingly the target audience for the co-branded card). But, surprisingly to many non-specialists, that is not the sole source of margin to reward cardholders with.

This is because, at the scale of the largest businesses in the world, financial services are cross-sold and structurally interconnected. There is one team in a bank (it happens to be Chase, for what it is worth) attempting to capture Starbuck’s card processing business. There is another team that wants to convince Starbucks to co-brand Chase card products. These two teams can talk to each other prior to making proposals to Starbucks.

And so, without knowing anything about the payments industry, you can speculate with a very high degree of confidence that Starbucks has received a complicated spreadsheet saying what Chase will charge it for every conceivable type of credit and debit card that wants a latte. A prominent negotiated line on that spreadsheet includes, effectively, a major discount for “on us” transactions: when Chase’s left hand needs to move money from Chase’s right hand because someone wants to pay Starbucks money for their Starbucks using their Starbucks-branded money. (This is easy to conflate with, and is separate from, Starbucks’ extremely impressive stored-value product. That probably mostly cannibalized their credit product, which… alright, we have to stop the levels of digression somewhere or we’ll be here all day.)

Because “on us” is structurally cheaper (the transaction literally travels over fewer rails and therefore there are fewer “mouths to feed”) and because it is incentive compatible for all parties to subsidize these transactions, as a card program designer, you have a relatively easy time being generous with regards to this particular cell of your spreadsheet.

Back to more complicated cases

So imagine you’re the card program designer for a card that, like most cards, does not have a particular named business happily subsidizing your users. You desire to quote a headline cashback number much higher than 1%. But you’d still like to keep some margin from interchange. What could you do?

One is you make the headline number larger but contingent on something. Say, for example, the card rebates 1.5%, but only for… bookstores. Any bookstore. For all other transactions, it is 1%.

The thing you would love with this offering is to preferentially attract people who are very emotionally invested in being readers and who spends very little of her on-this-card wallet on books. The emotional investment in the story the card offers brings the customer in; the blended cost to acquire the customer is closer to 1% industry standard and not to the 1.5% headline number.

Money is fungible, money is fungible, money is fungible, but many people don’t actually orient their lives as if this were true, and so the financial industry meets them where they are and then charges them for the privilege. This user values a dollar more when it is a books-dollar than when it is a food-dollar. You, a credit card program manager, can math out a way to get her as many books-dollars as she is interested in. (This is similar, in spirit, to how Bryrne Hobart describes airline frequent flyer programs as working. One key difference that credit card program managers have to understand: a source of advantage for frequent flyer miles as a pseudocurrency is that they can turn very-low-marginal-cost inputs, unsold seats, into very-high-perceived-marginal-benefit outputs, “free vacations”. Books-dollars may very well be worth more than a dollar to our target user here, but books-dollars are very difficult to manufacture in quantity for less than about 98ish cents.)

In principle, you could even offer more than your direct interchange revenue as the headline number, if you were very, very sure that your typical user would not preferentially use your card only to buy books and use a competitor’s card to buy groceries, gasoline, medicine, and similar.

Now, unfortunately, remember what we said about typical credit card users? That’s right. They don’t exist. Very many of your users will do what you want them to, and use the card in a perfectly-acceptable-but-not-exactly-optimal fashion, and you will have a blended cost very near 1% for them. And very many of your users will do exactly what you most don’t want, and use the card only to buy books.

This is… far less incentive compatible for you, particularly if you decided that the business of manufacturing books-dollars was so lucrative that you could rebate more than the direct interchange revenue given mix effects. These users will have blended costs very close to your headline number, not to your modeled blended costs.

These users will even band into tribes, find each other on the Internet, and swap tips for exploiting poor, defenseless credit card program managers like yourself. The tribal elders will eventually run businesses, with names like The Points Guy, which eventually get quietly acquired by very sophisticated private equity firms. Those PE firms are betting that you continue paying generous per-signup affiliate commissions to Internet properties which send you new card users. You bet you will also paying tens of millions of dollars annually to Frequently Adversely Selected New Accounts Dot Com. And Redditors bet they will continue chortling that they have pulled one over on you, because haha, you’re not nearly as good as they are at fourth grade math or keeping spreadsheets.

The biggest difference between you and a Redditor is not ability to do fourth grade math or ability to do spreadsheets. Redditors are frequently sophisticated with their spreadsheets; many of them could clearly earn three orders of magnitude more from the financial industry if they stopped thinking that the right way to monetize spreadsheet skill was in gaming credit card signup bonuses.

The biggest difference is that you’re optimizing over portfolios, over time and Redditors are largely playing in single player mode (and frequently over short horizons). You only care about single or dual player mode to the extent that you avoid obviously degenerate offerings where adverse selecting single players quickly dominate your entire book of business. Which is very much a risk, which is why the bank has smart people like you keeping spreadsheets.

The Redditors think failure modes for the bank sound like pudding guy. Pudding guy, was, of course, one of the highest-ROI ad buys in the history of capitalism.

Further refinements in cat and mouse games

But, just like lotteries have to keep reskinning the random number generators or the games get stale and ticket sales go down, credit card program managers have to periodically shake things up for something to cut through their adversaries’ built-in distribution networks and massive, massive marketing budgets.

One innovation, now 20+ years old, was a rotating favored category for cash-back. So instead of being 1.5% for bookstores 1% all else, it would be 1.5% for groceries in Q1, for gas in Q2, etc etc.

The theory behind this was pretty simple: many customers attracted by the headline number could be brought in the door by it but would be fairly inattentive after a card was their new “top of wallet” (the default card for spending). Over time, a combination of inattentiveness, changing willingness to spend time playing the game, and rewards caps would bring the portfolio’s cost of rewards close to the baseline and not to the headline reward number.

If for some reason playing this game interests you, one prominent product is called the Chase Freedom card. It should not be an attractive product for you, given plausible assumptions about the readership of this column, but it is an attractive enough product that probably millions of Americans use it.

Giving the customer more choices more frequently

If you were hypothetically to have spent the last few years dining with relatively well-off people in SFBA, when it came time to pay for dinner you’d see two credit card products with a combined 90%+ share: Chase Sapphire Reserve (CSR) and an interchangeable American Express card. This, ahem, includes many diners who are professionally connected to upstart payment methods.

American Express, for a very long time, had an almost mortal lock on the top end of the credit card market. Chase attempted to disrupt that in 2016 by very overtly attempting to buy away their core customer. You can read lots in other places about the original promotion, generally tsk-tsking about how absurdly lucrative it was for customers and how it caused Chase to have a (temporary) loss associated with their cards business. Personally, I think it was one of the most interesting strategic moves in the last 20 years of retail banking, but a full essay on that would require some other-than-public knowledge as to the size of the tsunami that happened after it.

One thing that is public but not well appreciated: Chase didn’t just decide to create an extremely lucrative-for-the-customer offering out of the goodness of their hearts and out of their own P&L. No, they pitched Visa on this idea. For too long, Visa, you have watched your competitor American Express outcompete every issuer in the Visa system for the best wallets in the world. They can do that because they can afford to, because American Express charges systematically higher interchange rates than Visa does even at its topmost tier. Visa, you should create a new tier where your not-exactly-chosen champions can try to spend those interchange dollars to give American Express a run for their money.

And, lo, Visa did create a new tier. You can expose yourself to gibbering madness if you want to know what the name for it is. But Chase got Visa to authorize Chase charging almost the entire economy more for credit card acceptance with the specific goal of outcompeting American Express for the most lucrative highest-monthly-spend virtually-never-revolve-a-balance credit card users.

That was part of what made the numbers work.

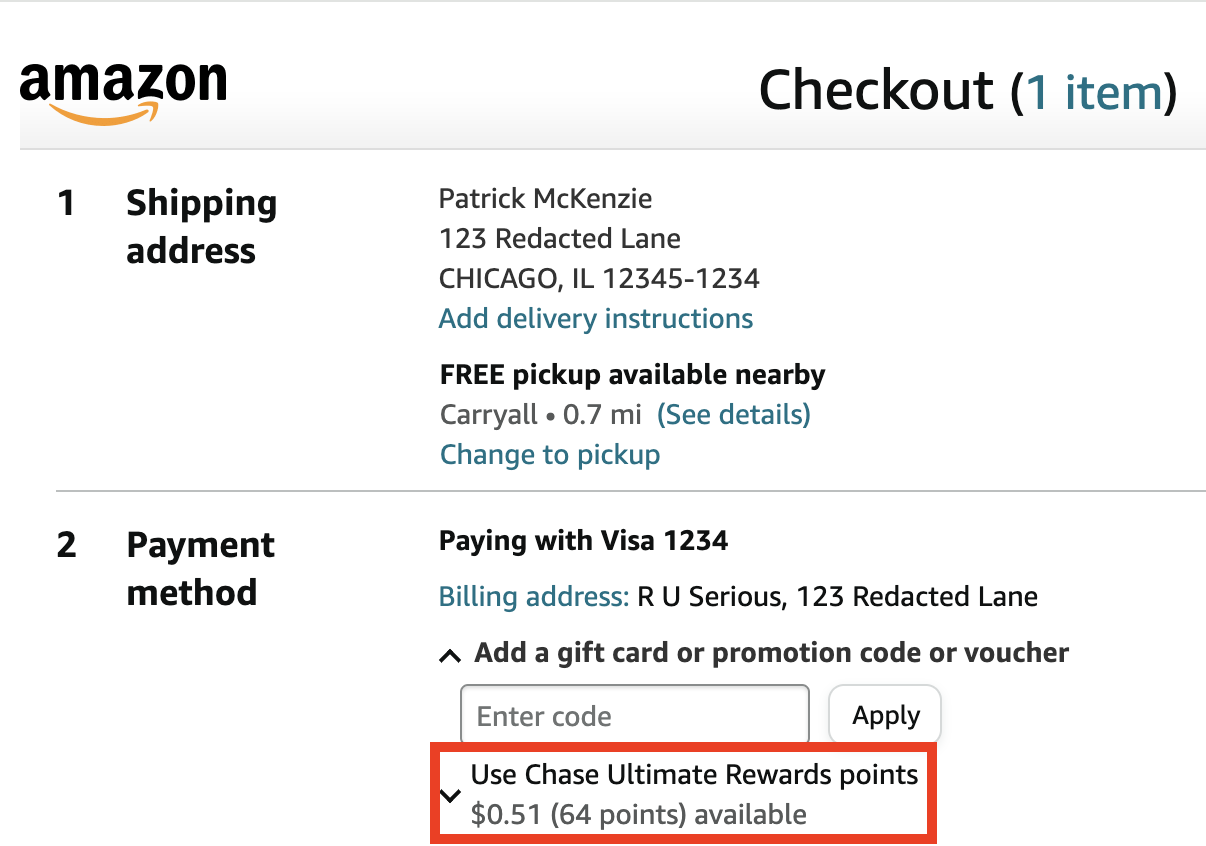

Another part is that the CSR offers a fairly complicated rewards scheme, with a lot of opportunities for people to pick things which feel great but are not optimal. For example, Chase will let you cash out CSR points on a 1:1 basis at either Amazon or Apple, integrated directly into the checkout flows. Those feel great.

People love Amazon and Apple and they love free Amazon and free Apple even more. This is true even among a portion of very sophisticated, wealthy, numerate CSR users, who love this idea so much they click a button designed for suckers.

Why is that a sucker’s checkout button? Because CSR also includes a feature called Pay Yourself Back which in the past prominently, and today a bit… less prominently, lets you cash out rewards at better than 1:1. You get a 25% bonus if you Pay Yourself Back by nominating past transactions at grocery stores: 10,000 points gets you $125 in statement credits if you are willing to do a trivial amount of clicking to show Chase $125+ in spend at grocery stores.

Stating the obvious: Chase knows what a computer is and does not require you to actually identify your purchases at grocery stores. This is a product decision to both a) force you to use your card at grocery stores and b) force yourself to say “Chase is getting me free groceries! How nice of them!” on a transaction-by-transaction level once a month to use your card optimally.

There are many, many other sucker buttons.

But, because the card is fundamentally targeted at rich, sophisticated people, Chase really does pay out a shedload of rewards. The 3% headline rate for travel and dining plus the 25% Pay Yourself Back kicker means there is a sustained and trivial pathway to get 375 bps out, which is one of the very, very, very few places in the industry where there is a sustained, trivial, uncapped way to get out more than the direct cost of interchange.

Why does this persist? Partly it is due to the standard credit card portfolio strategy: every time someone uses a CSR on Amazon (and not e.g. the Amazon rewards card, also from Chase) or uses CSR points to buy high-margin white plastic, Chase’s contribution margin for the portfolio goes up, and at scale quite a large percentage of customers do this.

Partly it is due to Chase thinking that they’ll just be so good for their target customer that their target customer will not bother playing the game optimally. That would require the customer carefully maintaining a portfolio of credit relationships and having seven cards saved on their iPhone and not, simply, the CSR.

Partly it is due to the really interesting strategic reasons for having CSR available: to a much larger degree than American Express, Chase is a diversified financial services empire. The CSR was effectively designed as a wedge product to get something Chase branded into the hands of affluent up-and-coming young urban professionals, with the goal of eventually getting them to not move just their wallet but their entire financial existence (and potentially their current-or-future entities’ financial existences) onto Chase.

The Sapphire mini-brand was so loved that they reused it for a bog-standard premium checking account. (It was named the Chase Sapphire Premium Checking Account, in a decision which probably consumed several tens of millions of dollars of professional effort, and I mean that absolutely descriptively and not as a criticism. I was not in that meeting… but I’ve been in that kind of meeting. Those that have been in it know that it is not in any way a single-meeting single-decisionmaker sort of call.)

More directions to go in

The blessing and curse of essays is that they have to end somewhere, and then pick up anew somewhere else. Hopefully the above gives you a bit more context on what is in your wallet.

In the future, we'll likely discuss the complicated iterated game played by the credit card networks and the rest of society regarding interchange rates, how there are high-interchange-high-reward equilibria and low-interchange-low-reward equilibria, the recent settlement where the networks agreed to temporarily decrease interchange, and other topics.

Want more essays in your inbox?

I write about the intersection of tech and finance, approximately biweekly. It's free.